Stress Testing:

A Practical Guide to Testing Resilience Under Severe Pressure

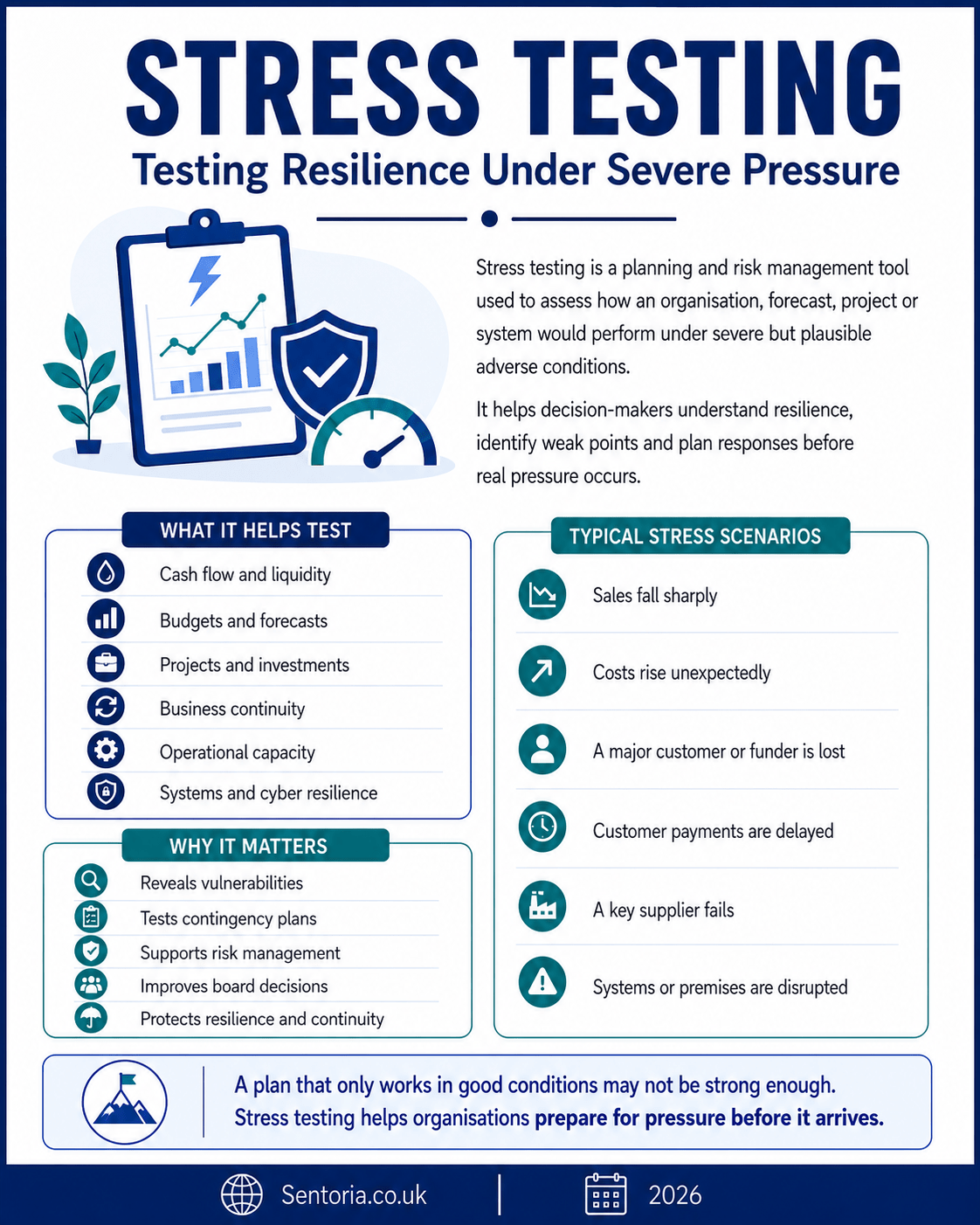

Stress testing is a planning, risk management and decision-making tool used to test how an organisation, project, forecast, system or strategy would perform under difficult, severe or adverse conditions.

At its simplest, stress testing asks:

What happens if things get significantly worse than expected, and could we still cope?

That makes it useful for business planning, cash flow management, forecasting, risk management, charity governance, public sector planning, banking, property development, construction, manufacturing, cyber security, business continuity, project management and board reporting.

Used properly, stress testing helps organisations understand whether their plans are resilient enough. It does not predict that a severe event will happen. It tests whether the organisation could survive, adapt or recover if it did.

What is stress testing?

Stress testing examines the effect of severe but plausible adverse conditions.

It tests what would happen if important assumptions moved sharply against the organisation.

For example:

- Sales fall by 25%.

- A major customer is lost.

- A key grant is not renewed.

- Interest rates rise materially.

- Build costs increase by 15%.

- A critical supplier fails.

- Customer payments are delayed by 60 days.

- A cyber attack disrupts operations.

- Staff absence rises sharply.

- Energy costs increase significantly.

- A project is delayed by six months.

- Demand for a service rises beyond capacity.

- A major tenant defaults.

- Funding is delayed.

- A regulatory change increases costs.

The aim is to understand:

- What would break first?

- How much headroom exists?

- Which assumptions are most dangerous?

- Which risks could combine?

- Which controls would be tested?

- What early warning signs should be monitored?

- What actions would be needed?

- Whether the organisation remains within risk appetite.

- Whether contingency plans are strong enough.

- Whether the strategy is still viable.

Stress testing is especially useful when normal forecasts look acceptable but management needs to know what happens under pressure.

Stress testing, sensitivity analysis and scenario analysis

Stress testing is closely related to sensitivity analysis and scenario analysis, but it is not the same.

Sensitivity analysis

Sensitivity analysis changes one assumption at a time.

It asks:

What happens if this assumption changes?

Example:

What happens if sales fall by 10%?

Scenario analysis

Scenario analysis changes several assumptions together to create a plausible alternative future.

It asks:

What happens under this different set of circumstances?

Example:

What happens if sales fall by 10%, costs rise by 5%, and customer payments slow by 15 days?

Stress testing

Stress testing applies more severe pressure to test resilience.

It asks:

What happens under serious adverse conditions, and can we survive or recover?

Example:

What happens if sales fall by 25%, a major customer pays late, costs rise, and bank facilities are reduced?

In simple terms:

Sensitivity analysis tests movement.

Scenario analysis tests alternative futures.

Stress testing tests resilience under pressure.

All three are useful. They answer different questions.

History and development of stress testing

Stress testing developed from risk management, banking, financial modelling, engineering, insurance, project appraisal and resilience planning.

Its use became especially prominent in banking and financial services because regulators, boards and investors needed to understand whether institutions could withstand serious economic shocks.

However, the principle is much wider than banking.

Any organisation can fail if a plan is only tested against comfortable assumptions.

A business may look profitable until a major customer is lost.

A charity may look sustainable until a grant is withdrawn.

A property development may look viable until build costs rise and completion is delayed.

A public service may look adequately resourced until demand increases sharply.

A software platform may look stable until usage spikes or systems fail.

A business continuity plan may look credible until the organisation tests whether people can actually operate without its normal systems.

Stress testing developed because decision-makers need to understand not only what is expected, but what could happen under pressure.

The key idea is simple:

A plan that only works in good conditions may not be strong enough.

Why stress testing matters

Stress testing matters because organisations often underestimate downside risk.

Plans can become too optimistic. Forecasts can assume normal conditions. Budgets can assume income arrives on time. Projects can assume costs remain stable. Strategies can assume markets behave sensibly. Boards can receive reports that show a base case without understanding the downside.

Stress testing helps challenge that.

It supports:

- Better risk management

- Stronger cash flow planning

- Better board and trustee oversight

- More realistic forecasts

- Better business continuity planning

- Stronger investment appraisal

- Better understanding of financial headroom

- Earlier warning of emerging risk

- Better contingency planning

- Improved strategic resilience

- More honest decision-making

- Stronger lender or funder conversations

- Better internal audit focus

- Better assessment of risk appetite

- Reduced false confidence

Stress testing is not about being pessimistic.

It is about being prepared.

A sensible organisation does not only ask:

What do we expect to happen?

It also asks:

What would we do if things turned against us?

When to use stress testing

Stress testing is useful whenever an organisation needs to understand resilience under pressure.

Common uses include:

- Cash flow planning

- Budget approval

- Business planning

- Investment appraisal

- Property development

- Construction projects

- Charity reserves planning

- Public sector financial planning

- Bank lending assessments

- Covenant testing

- Strategic planning

- Business continuity planning

- Project approval

- Cyber resilience

- Supplier dependency review

- Workforce planning

- Service demand planning

- Risk appetite review

- Board reporting

- Scenario planning

It is especially useful where:

- The decision is material.

- The downside could be serious.

- Financial headroom is limited.

- Income is uncertain.

- Costs are volatile.

- Delivery depends on third parties.

- A project is long-term.

- There are major assumptions.

- The organisation has legal or safeguarding duties.

- Failure would damage reputation or continuity.

It is less useful when used as a theoretical exercise with no link to action.

What can be stress tested?

Stress testing can be applied to many different areas.

Financial forecasts

Financial forecasts can be stress tested for:

- Lower sales

- Delayed customer receipts

- Higher costs

- Lower margins

- Higher interest rates

- Reduced funding

- Higher bad debts

- Lower occupancy

- Higher payroll costs

- Loss of a major customer

This helps assess solvency, cash headroom, reserves, covenant compliance and financial sustainability.

Cash flow

Cash flow stress testing is especially important.

A business can be profitable but still run out of cash.

Cash stress tests may include:

- Major debtor paying 60 days late.

- Sales receipts falling sharply.

- Supplier payment terms tightening.

- VAT or tax payment being higher than expected.

- Payroll costs rising.

- Loan repayments increasing.

- Capital expenditure being required earlier.

- Stock tying up more cash.

- Grant income being delayed.

- Emergency costs arising.

Cash flow is often where stress appears first.

Projects

Project stress testing may include:

- Cost overruns

- Programme delay

- Contractor failure

- Key staff loss

- Scope changes

- Supplier failure

- Planning delay

- Funding delay

- Inflation

- Stakeholder challenge

This helps test whether contingencies, governance and escalation arrangements are strong enough.

Business continuity

Business continuity stress testing asks whether the organisation could continue operating during disruption.

It may test:

- Loss of premises

- IT outage

- Cyber attack

- Staff absence

- Supplier failure

- Utilities failure

- Communication breakdown

- Data loss

- Transport disruption

- Loss of key records

A business continuity plan that has not been stress tested may be only a paper plan.

Systems and technology

Technology stress testing may examine:

- System load

- Cyber attack response

- Data recovery

- Backup restoration

- Cloud provider failure

- Failed software release

- Integration failure

- Support capacity

- User spike

- Security incident

For technology businesses, stress testing can reveal whether systems are resilient enough before customers experience failure.

Strategy

Strategic stress testing asks whether the organisation’s strategy still works under adverse conditions.

It may test:

- Economic downturn

- Market decline

- Competitor disruption

- Funding reduction

- Regulation change

- Technology shift

- Customer behaviour change

- Supply chain disruption

- Workforce shortage

- Reputational event

This is useful for boards and leadership teams because it challenges whether the strategy is robust.

Stress testing in different industries

SMEs and owner-managed businesses

For SMEs, stress testing should focus on survival, cash and operational resilience.

Small businesses often have limited financial headroom. They may depend on a small number of customers, a few key staff, a limited supplier base, or one owner-manager.

Typical SME stress tests include:

- Sales fall by 25%.

- Largest customer is lost.

- Largest customer pays 60 days late.

- Gross margin falls by 5%.

- Payroll costs rise by 10%.

- A key employee leaves.

- A supplier demands payment upfront.

- Bank facilities are reduced.

- VAT payment coincides with lower receipts.

- The owner is unavailable for four weeks.

An SME might ask:

- How long can we survive with lower sales?

- What cash headroom do we have?

- Which costs can be reduced quickly?

- Which customers create concentration risk?

- Which suppliers are critical?

- What would happen if the owner could not work?

- What early warning signs should we track?

- What action should we take now?

For SMEs, stress testing should be practical. It should lead to specific actions around cash, customers, costs, staffing and contingency.

Manufacturing

Manufacturing businesses need stress testing because operations depend on demand, materials, labour, energy, machinery and supply chains.

Typical manufacturing stress tests include:

- Raw material costs increase by 15%.

- Energy costs increase sharply.

- A critical supplier fails.

- Production volume falls by 20%.

- A major machine is unavailable for two weeks.

- Scrap rate doubles.

- Customer demand changes suddenly.

- Labour availability falls.

- Transport disruption delays delivery.

- A product recall is required.

A manufacturer might ask:

- Which inputs create the greatest exposure?

- What happens if material costs rise?

- How long can production continue without a key supplier?

- What stock buffer is needed?

- What happens if machinery downtime increases?

- Can customers be served from alternative production routes?

- What happens to cash if stock builds up?

- Which controls need strengthening?

For manufacturing, stress testing should connect production, finance, procurement, maintenance and customer delivery.

Retail and ecommerce

Retail and ecommerce businesses are exposed to customer demand, stock risk, returns, delivery, online platforms and advertising costs.

Typical stress tests include:

- Website outage during peak period.

- Conversion rate falls by 30%.

- Advertising cost per sale doubles.

- Return rate increases sharply.

- Stock arrives late.

- Supplier prices rise by 10%.

- Delivery partner fails.

- Marketplace account is suspended.

- Customer demand falls after stock is purchased.

- Negative reviews reduce conversion.

A retailer might ask:

- What happens if peak sales underperform?

- What happens if stock cannot be sold at full price?

- What happens if returns increase?

- What happens if online advertising becomes uneconomic?

- What happens if the website fails?

- How much cash is tied up in stock?

- What customer communication plan is needed?

- Which products are most exposed?

For ecommerce, stress testing should include both revenue and margin. Sales volume alone is not enough.

Professional services

Professional services firms need stress testing around clients, staffing, deadlines, work in progress, billing and professional risk.

Typical stress tests include:

- Major client leaves.

- Debtor days increase by 30 days.

- Staff utilisation falls.

- Fixed-fee work overruns.

- Key partner or manager leaves.

- Professional indemnity premium increases.

- Regulatory deadline pressure increases.

- Software failure affects client delivery.

- Work in progress cannot be billed.

- Client pipeline conversion falls.

For accountants, solicitors, consultants, architects and advisers, stress testing can ask:

- What happens if a major client leaves?

- What level of utilisation is needed to cover costs?

- What happens if clients pay late?

- What happens if staff costs rise?

- What happens if a deadline is missed?

- How much work in progress is recoverable?

- Which services are most resilient?

- Which clients create the most exposure?

Professional services stress testing should link profitability, capacity, quality and cash collection.

Charities and voluntary organisations

Charities need stress testing because they often face uncertain income, rising demand and limited reserves.

Typical charity stress tests include:

- Major grant not renewed.

- Donation income falls by 20%.

- Payroll costs rise by 8%.

- Service demand increases by 30%.

- Restricted funding fails to cover full costs.

- Reserves fall below policy level.

- Volunteer availability reduces.

- Funder payment is delayed.

- Public sector contract is reduced.

- Safeguarding or reputational incident occurs.

A charity might ask:

- How long will reserves last under a deficit?

- Which services are most financially exposed?

- What happens if a major funder withdraws?

- What happens if demand rises while income falls?

- Which costs are fixed?

- Which services could be protected?

- What trigger points require trustee action?

- What early action is needed?

For charities, stress testing should be linked to reserves policy, risk appetite, funding strategy, service impact and trustee oversight.

Public sector and local government

Public bodies use stress testing to understand service, budget and demand pressures.

Typical stress tests include:

- Demand for statutory services rises sharply.

- Savings plans are delayed.

- Inflation exceeds budget assumptions.

- Contract costs increase.

- Grant funding reduces.

- Contractor fails.

- Workforce absence increases.

- Major IT system fails.

- Legal challenge delays delivery.

- Public demand rises during an emergency.

A public body might ask:

- What happens if demand rises above forecast?

- What happens if savings are not delivered?

- Which statutory services are most exposed?

- What happens if contractors fail?

- What level of reserves or contingency is required?

- Which services would need prioritisation?

- Which decisions need member or board approval?

- What are the public value implications?

For public sector work, stress testing should be transparent, evidence-based and linked to governance.

Property and construction

Property and construction projects are highly suited to stress testing because they involve long timescales, high cost and major uncertainty.

Typical stress tests include:

- Build costs increase by 15%.

- Planning approval is delayed by nine months.

- Interest rates rise.

- Rental values fall.

- Sales values fall.

- Occupancy is lower than expected.

- Contractor becomes insolvent.

- Utilities connection is delayed.

- Funding terms tighten.

- Exit yield moves adversely.

A property appraisal might ask:

- What happens if costs rise?

- What happens if rents are lower?

- What happens if completion is delayed?

- What happens if interest rates increase?

- What happens if sales take longer?

- What is the minimum viable rent or sale value?

- How much contingency is needed?

- At what point does the project become unviable?

For property and construction, stress testing should be part of viability appraisal, board approval and ongoing project review.

Technology and software

Technology businesses need stress testing around growth, systems, cyber risk, customer behaviour and cash runway.

Typical stress tests include:

- Customer acquisition cost doubles.

- Churn increases sharply.

- Monthly recurring revenue growth slows.

- Hosting costs rise with usage.

- Product launch is delayed.

- Key developer leaves.

- System outage affects customers.

- Cyber attack disrupts operations.

- Funding round is delayed.

- Support tickets increase beyond capacity.

A software business might ask:

- How long is the cash runway under lower growth?

- What happens if churn rises?

- What happens if customer acquisition becomes more expensive?

- What happens if the product takes longer to develop?

- Can systems cope with a usage spike?

- What happens if the platform fails?

- What customer communication plan is needed?

- Which metrics provide early warning?

For technology businesses, stress testing should cover both financial resilience and operational resilience.

Healthcare and social care

Healthcare and social care organisations need stress testing because safety, staffing, demand and continuity matter.

Typical stress tests include:

- Staff absence increases sharply.

- Agency costs rise.

- Occupancy falls.

- Demand rises above planned capacity.

- Funding rates do not match wage costs.

- Medication system fails.

- Care records become unavailable.

- Safeguarding incident requires urgent action.

- Inspection outcome creates improvement costs.

- Supplier failure affects care delivery.

A care provider might ask:

- What happens if staffing falls below planned levels?

- What happens if agency costs rise?

- What happens if occupancy falls?

- What happens if care needs increase?

- Can safe service levels be maintained?

- What happens if key systems are unavailable?

- What escalation routes exist?

- What contingency is needed?

In healthcare and care, stress testing should support safety, quality, safeguarding and continuity. It should never be used to justify unsafe levels of service.

Education and training

Education providers can use stress testing for learner numbers, funding, staffing, safeguarding, course viability and technology.

Typical stress tests include:

- Enrolment falls by 20%.

- Funding rates reduce.

- Completion rates fall.

- Tutor absence increases.

- Digital platform fails.

- Employer placements reduce.

- Learner support needs increase.

- Assessment deadlines are delayed.

- Inspection creates additional requirements.

- Safeguarding pressures increase.

An education provider might ask:

- How many learners are needed for a course to remain viable?

- What happens if enrolments are lower?

- What happens if funding is reduced?

- What happens if completion rates fall?

- What staffing contingency exists?

- What happens if online delivery fails?

- What support pressures could increase?

- Which courses or programmes are most exposed?

For education, stress testing should link financial sustainability with learner outcomes, safeguarding and quality.

How to carry out stress testing properly

1. Define the purpose

Start by deciding why the stress test is being done.

Possible purposes include:

- Test cash resilience.

- Test business continuity.

- Test project viability.

- Test financial sustainability.

- Test risk appetite.

- Test a strategic plan.

- Test an investment proposal.

- Test reserves adequacy.

- Test operational capacity.

- Test system resilience.

A stress test should support a decision.

Without a clear purpose, it becomes a theoretical exercise.

2. Define the object being tested

Be clear about what is being stress tested.

It may be:

- A cash flow forecast

- A budget

- A business plan

- A project

- A property appraisal

- A charity reserves plan

- A service model

- A technology platform

- A business continuity plan

- A strategic plan

The stress test should match the object.

For example, a cash flow stress test should focus on receipts, payments, headroom and timing. A service stress test should focus on capacity, quality, staffing and continuity.

3. Identify key vulnerabilities

Before applying a stress, identify where the plan is vulnerable.

Ask:

- What assumptions matter most?

- What could change quickly?

- What are we dependent on?

- Where is financial headroom limited?

- Which costs are fixed?

- Which income is uncertain?

- Which suppliers are critical?

- Which people are essential?

- Which systems are critical?

- Which risks are already high?

This helps ensure the stress test focuses on the right pressures.

4. Design severe but plausible stresses

A stress test should be challenging, but not absurd.

Examples include:

- Sales fall by 25%.

- Customer receipts are delayed by 60 days.

- Build costs rise by 15%.

- A major funder withdraws.

- A key supplier fails.

- Staff absence doubles.

- Interest rates rise by 2%.

- System outage lasts three days.

- Service demand rises by 30%.

- Major customer contract is lost.

The stress should be severe enough to reveal weakness.

If the stress is too mild, it may provide false reassurance.

5. Test individual and combined stresses

Some stress tests examine one severe event.

Others combine several pressures.

For example:

Single stress: Sales fall by 25%.

Combined stress: Sales fall by 25%, debtor days increase by 30 days, and costs rise by 8%.

Combined stresses are often more realistic because adverse events can interact.

For example, an economic downturn may reduce sales, increase bad debts, tighten credit and increase pressure on cash at the same time.

6. Calculate the impact

The stress test should show the effect clearly.

Possible outputs include:

- Closing cash balance

- Minimum cash headroom

- Profit or loss

- Reserves level

- Funding gap

- Debt covenant position

- Break-even point

- Project viability

- Service capacity

- Recovery time

- Staffing shortfall

- System downtime

- Customer impact

- Regulatory impact

- Reputation impact

The output should be relevant to the decision.

For example, if the question is survival, cash headroom may matter more than accounting profit.

7. Identify breaking points

Stress testing should identify where the organisation or plan fails.

Breaking points may include:

- Cash falls below zero.

- Reserves fall below policy level.

- Debt covenants are breached.

- Service standards cannot be maintained.

- Staffing levels become unsafe.

- Project return becomes negative.

- Contingency is exhausted.

- System recovery exceeds tolerance.

- Regulatory deadlines cannot be met.

- Risk appetite is exceeded.

This is one of the most valuable parts of stress testing.

It shows how much pressure the organisation can absorb.

8. Identify early warning indicators

A good stress test should identify warning signs.

Examples include:

- Sales enquiries falling

- Conversion rate reducing

- Debtor days increasing

- Cash headroom reducing

- Grant decisions delayed

- Supplier lead times increasing

- Staff absence rising

- Project milestones slipping

- Support tickets increasing

- Customer complaints rising

- Stock turn slowing

- Covenant headroom reducing

- Website performance weakening

- Demand exceeding capacity

- Reserves falling

Early warning indicators help management act before the stress fully arrives.

9. Agree management actions

Stress testing should lead to action.

Possible actions include:

- Reduce discretionary spending.

- Increase cash monitoring.

- Renegotiate supplier terms.

- Strengthen credit control.

- Build reserves.

- Reduce customer concentration.

- Secure alternative suppliers.

- Increase contingency.

- Pause or re-scope a project.

- Strengthen business continuity plans.

- Update the risk register.

- Adjust risk appetite.

- Review staffing plans.

- Improve cyber controls.

- Prepare stakeholder communication.

A stress test without action is only information.

10. Report and review

Stress testing should be reported clearly to the right audience.

For example:

- Management team

- Board

- Trustees

- Audit committee

- Risk committee

- Finance committee

- Project board

- Lender

- Funder

- Regulator where relevant

The report should explain:

- Purpose

- Base case

- Stress applied

- Result

- Breaking point

- Key risks

- Mitigating actions

- Decisions required

- Owner

- Review date

Stress tests should be updated when conditions change.

Common stress testing techniques

Reverse stress testing

Reverse stress testing starts with failure and works backwards.

It asks:

What would have to happen for the organisation, project or plan to fail?

For example:

- What would cause cash to run out?

- What would make the project unviable?

- What would cause reserves to fall below policy?

- What would cause service failure?

- What would cause a covenant breach?

- What would make the strategy fail?

Reverse stress testing is useful because it identifies critical vulnerabilities.

It can be more revealing than simply applying a standard downside case.

Severe but plausible scenario

This method creates a realistic but challenging adverse scenario.

For example:

A downturn reduces sales by 20%, customer payments slow by 30 days, and gross margin falls by 3%.

This helps test whether the organisation can survive a difficult but credible situation.

Combined stress test

A combined stress test applies several adverse movements at once.

For example:

- Income falls

- Costs rise

- Cash receipts slow

- Funding is delayed

- Project costs increase

This is useful because real-world pressures often happen together.

Liquidity stress test

A liquidity stress test focuses on cash.

It asks:

Can the organisation meet payments as they fall due under stress?

This is especially important for SMEs, charities, property businesses, construction projects and highly leveraged organisations.

Operational stress test

An operational stress test focuses on delivery capacity.

It asks:

Can we continue operating if people, systems, suppliers or premises are disrupted?

This is useful for business continuity planning.

Technology stress test

A technology stress test examines whether systems can cope with pressure.

It may include:

- Load testing

- Cyber incident simulation

- Backup restoration

- Disaster recovery testing

- Access failure testing

- Supplier outage simulation

This is essential for digital businesses and organisations dependent on IT.

Common mistakes in stress testing

Mistake 1: Making the stress too mild

If the stress is comfortable, it will not reveal much.

A stress test should challenge the plan.

Mistake 2: Using unrealistic shocks

The stress should be severe but plausible.

If it is completely unrealistic, decision-makers may ignore it.

Mistake 3: Ignoring combined effects

Many pressures happen together.

Testing one issue at a time may understate the real danger.

Mistake 4: Focusing only on profit

Profit is important, but cash, capacity, compliance, service quality and reputation may matter more under stress.

Mistake 5: Ignoring timing

Timing can be critical.

A business may survive a loss over a year but fail if cash outflows happen before receipts.

Mistake 6: Not identifying breaking points

A stress test should show where the plan fails.

Without that, the organisation may not understand its true limits.

Mistake 7: Not linking to action

Stress testing should lead to decisions.

If no action follows, the test has limited value.

Mistake 8: Ignoring risk appetite

A plan may survive a stress but still move outside risk appetite.

For example, reserves may fall below the agreed minimum.

Mistake 9: Not involving the right people

Finance may understand the numbers, but operations, sales, HR, IT, safeguarding and service teams may understand the practical consequences.

Stress testing should involve relevant people.

Mistake 10: Not updating the test

A stress test becomes stale when assumptions change.

It should be reviewed regularly.

Limitations and weaknesses of stress testing

Stress testing is useful, but it has limits.

It does not predict the future

A stress test does not say the stress will happen.

It shows what would happen if it did.

It depends on the stress chosen

If the wrong stress is selected, the analysis may miss the real vulnerability.

It depends on model quality

A stress test cannot fix a poor model.

If the forecast, cash flow or project appraisal is wrong, the stress test may also be wrong.

It can create false confidence

Passing one stress test does not mean the organisation is safe.

Other stresses may still cause serious problems.

It can be too financial

Some stress tests focus only on numbers and miss operational, legal, people, safeguarding or reputational impacts.

It can be too pessimistic if misused

Stress testing should inform decisions, not paralyse them.

The aim is resilience, not fear.

It can be ignored

If the findings are uncomfortable, organisations may avoid acting.

Leadership and governance matter.

It does not replace judgement

Stress testing supports decision-making.

It does not make decisions by itself.

Stress testing compared with other strategic and management tools

Stress testing and sensitivity analysis

Sensitivity analysis tests how changes in assumptions affect outcomes.

Stress testing applies more severe adverse conditions.

Use sensitivity analysis to understand key drivers. Use stress testing to test resilience.

Stress testing and scenario planning

Scenario planning explores different plausible futures.

Stress testing examines whether the organisation can withstand a severe adverse situation.

Use scenario planning for strategic uncertainty. Use stress testing for resilience.

Stress testing and forecasting

Forecasting estimates likely outcomes.

Stress testing tests what happens if the forecast is badly wrong or conditions deteriorate.

Use forecasting for the base case. Use stress testing for downside resilience.

Stress testing and assumptions log

Stress testing identifies assumptions that could create serious exposure.

Those assumptions should be recorded, owned and reviewed in the assumptions log.

Stress testing and risk register

Stress testing can reveal risks or increase risk ratings.

The results should feed into the risk register, risk matrix and action planning.

Stress testing and risk appetite statement

Stress testing helps assess whether adverse conditions would push the organisation outside appetite.

For example, cash reserves, service standards or cyber recovery times may breach tolerance limits.

Stress testing and business continuity plan

Business continuity planning explains how operations will continue during disruption.

Stress testing checks whether those plans work under pressure.

Stress testing and internal audit

Internal audit can review whether stress testing is being performed, whether assumptions are reasonable and whether actions are followed up.

Stress testing and bow-tie analysis

Bow-tie analysis maps causes, consequences and controls.

Stress testing can test whether those controls are strong enough under severe conditions.

Stress testing and investment appraisal

Investment appraisal assesses whether a project is worthwhile.

Stress testing assesses whether the project remains viable under adverse conditions.

Alternatives and complementary frameworks

Sensitivity analysis

Use sensitivity analysis to test individual assumptions.

Best used before stress testing to identify the most important drivers.

Scenario analysis

Use scenario analysis to test plausible combinations of assumptions.

Best used for alternative future conditions.

Reverse stress testing

Use reverse stress testing to identify what would cause failure.

Best used when resilience and survival are central.

Business continuity planning

Use business continuity planning to prepare operational responses to disruption.

Best used where continuity of services, systems or sites matters.

Risk register

Use the risk register to record and manage risks identified through stress testing.

Assumptions log

Use an assumptions log to record key assumptions tested under stress.

Forecasting

Use forecasting to create the base case that stress testing challenges.

Cash flow modelling

Use cash flow modelling to test liquidity under pressure.

Best used for SMEs, charities, property projects and organisations with limited headroom.

Monte Carlo simulation

Use Monte Carlo simulation where many variables interact and probability ranges are useful.

Best used for complex financial, project or risk modelling.

A practical stress testing template

A useful stress testing template should include:

- Stress test name

- Purpose

- Area tested

- Base case

- Key assumptions

- Stress applied

- Reason for stress

- Output measure

- Result under stress

- Breaking point

- Minimum headroom

- Risk appetite impact

- Early warning indicators

- Mitigating actions

- Contingency actions

- Owner

- Decision required

- Link to risk register

- Review date

- Version control

Example:

Stress test: 13-week cash flow downside stress

Purpose: Test whether the business can meet payroll, VAT, suppliers and loan repayments if receipts are delayed.

Base case: Minimum cash headroom of £85,000.

Stress applied: Sales receipts fall by 20%, largest customer payment of £75,000 delayed by six weeks, and supplier payments remain due on original terms.

Result: Minimum cash headroom falls to £12,000 in week seven.

Breaking point: Cash becomes negative if one additional customer payment above £20,000 is delayed.

Risk appetite impact: Cash headroom is below the board’s minimum tolerance of £50,000.

Actions: Increase credit control, delay non-essential expenditure, discuss temporary facility with bank, review supplier payment timing, update weekly cash monitoring.

Owner: Finance Director.

Review date: Weekly until headroom improves.

Questions to ask during stress testing

Purpose questions

- What are we trying to test?

- What decision will this support?

- Who needs the results?

- What would make the stress test useful?

- Is this about survival, resilience, viability or control?

- What area is most exposed?

- What time period matters?

- What output matters most?

- What action may follow?

- How often should the test be repeated?

Stress design questions

- What severe but plausible event should we test?

- What has happened before?

- What is happening in the sector?

- What risks are already high?

- What assumptions are most uncertain?

- What would cause the greatest pressure?

- Which risks could happen together?

- Are we testing enough downside?

- Is the stress realistic?

- Is the stress challenging enough?

Financial questions

- What happens to cash?

- What happens to profit?

- What happens to reserves?

- What happens to debt?

- What happens to covenant headroom?

- What happens to working capital?

- What happens to funding?

- What costs become unavoidable?

- What costs can be reduced?

- What is the breaking point?

Operational questions

- Can critical activities continue?

- Which services would be affected?

- Which staff are essential?

- Which systems are essential?

- Which suppliers are critical?

- What workarounds exist?

- Are workarounds realistic?

- What capacity is available?

- What quality risks arise?

- What customer or service user impact occurs?

Risk questions

- Which risks become more serious?

- Which controls are tested?

- Which controls may fail?

- Does the stress move us outside risk appetite?

- Which risks should be escalated?

- Which risks need more mitigation?

- Which assumptions need monitoring?

- Which early warning indicators matter?

- What contingency is required?

- What should be added to the risk register?

Action questions

- What should we do now?

- What action would be taken if the stress begins?

- Who owns the action?

- What trigger point starts the action?

- What decision is needed?

- Is board approval required?

- Is external support needed?

- Should spending be paused?

- Should the plan be changed?

- When will this be reviewed?

The best way to think about stress testing

Stress testing is not about predicting disaster.

It is about testing resilience.

A good stress test should be:

- Clear

- Severe but plausible

- Linked to a decision

- Based on key vulnerabilities

- Evidence-informed

- Connected to risk appetite

- Focused on breaking points

- Linked to action

- Reviewed regularly

- Understood by decision-makers

A weak stress test says:

“Here is a downside number.”

A strong stress test asks:

“What would happen under serious pressure, where would we break, and what action should we take now?”

The key question is not simply:

Can we survive this stress?

The better question is:

What does this stress reveal about our cash, capacity, controls, risks and readiness?

Conclusion: stress testing turns resilience from assumption into evidence

Stress testing remains useful because every plan looks stronger before it is put under pressure.

Forecasts can look healthy. Projects can look viable. Budgets can appear balanced. Strategies can feel robust. Business continuity plans can look complete.

The real question is whether they still work when conditions deteriorate.

Used badly, stress testing becomes a pessimistic spreadsheet exercise that produces numbers but no decisions.

Used properly, it becomes a practical management tool. It helps organisations identify vulnerabilities, test resilience, challenge assumptions, protect cash, improve risk management and prepare contingency plans.

The real value is not in creating a severe scenario.

The real value is in understanding what the severe scenario reveals.

A strong stress testing process helps an organisation move from saying, “We think we can cope,” to asking, “What evidence do we have, where are we exposed, and what should we do before the pressure arrives?”